Luxury Watch Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 54.18 Billion |

| Market Size (2030) | USD 72.98 Billion |

| Growth Rate (2025 - 2030) | 6.14% CAGR |

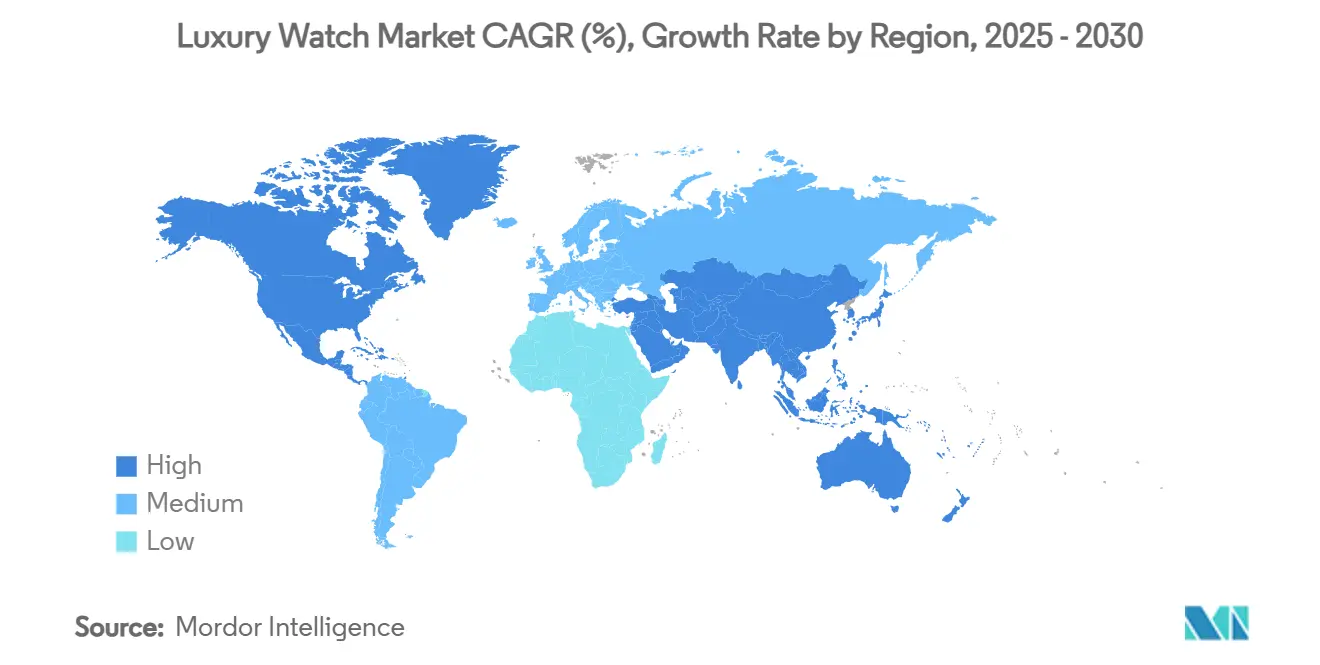

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Watch Market Analysis by Mordor Intelligence

The luxury watch market size is estimated at USD 54.18 billion in 2025, and is expected to reach USD 72.98 billion by 2030, at a CAGR of 6.14% during the forecast period (2025-2030). Luxury watchmakers are riding a wave of growth, blending age-old craftsmanship with modern technology, all while catering to a consumer shift towards premium, heritage-rich timepieces. Major players, like Audemars Piguet and Rolex, bolster their market stance with limited-edition and bespoke designs, drawing in high-net-worth individuals and collectors. E-commerce's rise, coupled with a swell in global wealth and burgeoning demand from markets like China, India, and the Middle East, fuels this expansion. In regions like Asia-Pacific and North America, there's a pronounced appetite for watches adorned with precious metals, intricate mechanical movements, and sleek designs. The industry's pivot towards sustainable materials, combined with high-profile partnerships with fashion icons, celebrities, and artists, resonates deeply with the younger affluent demographic. Additionally, the integration of smart features into luxury watches is gaining traction, appealing to tech-savvy consumers without compromising on traditional aesthetics. The growing trend of pre-owned luxury watches is also contributing to market growth, as it offers affordability and access to rare models. Furthermore, the increasing use of digital marketing strategies, including social media campaigns and influencer collaborations, is enhancing brand visibility and consumer engagement. The market is also witnessing a rise in exclusive in-store experiences and personalized services, which further strengthen customer loyalty. Despite hurdles like premium pricing and counterfeiting, the market stands firm, rooted in its commitment to exclusivity, innovation, and time-honored craftsmanship.

Key Report Takeaways

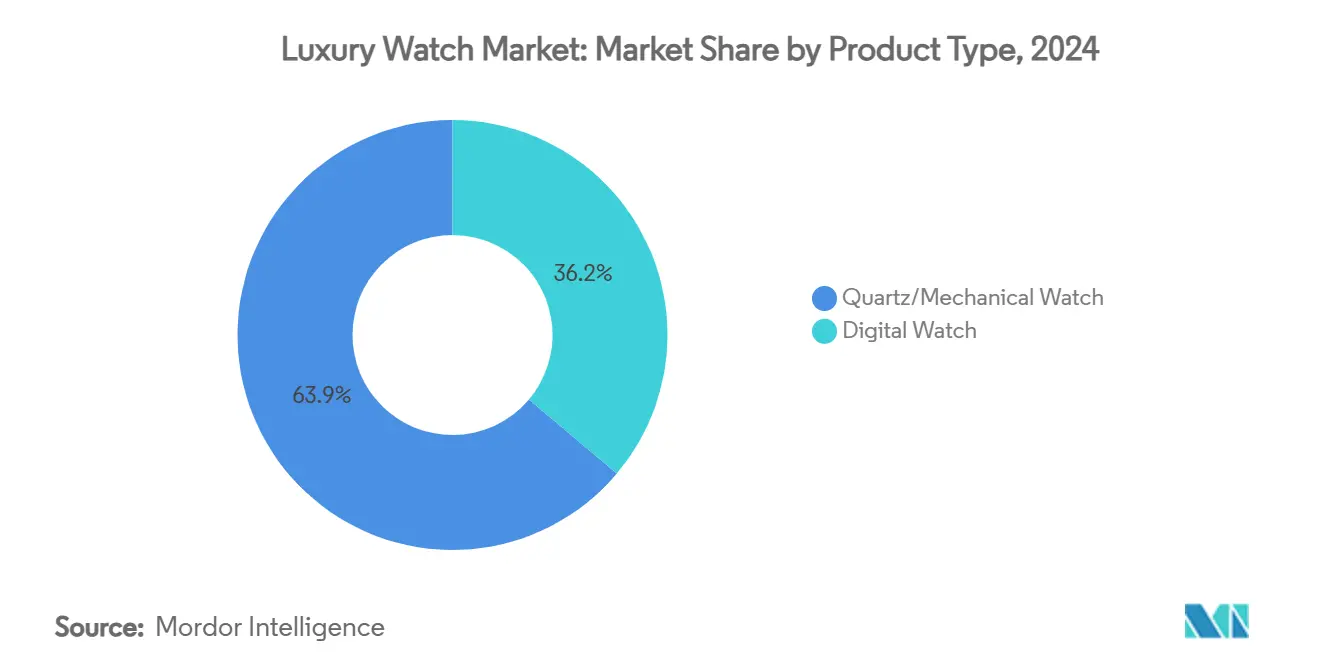

- By product type, quartz/mechanical watches led with 63.85% of the luxury watch market share in 2024; digital watches are projected to advance at a 6.42% CAGR to 2030.

- By end user, men held 51.88% share of the luxury watch market in 2024, while the women’s segment is forecast to expand at a 6.75% CAGR through 2030.

- By distribution channel, offline stores commanded 66.82% of the luxury watch market size in 2024; online stores are set to grow at a 7.01% CAGR between 2025-2030.

- By geography, Asia-Pacific accounted for 40.51% of the luxury watch market share in 2024, whereas South America is projected to post a 7.63% CAGR over the same horizon.

Global Luxury Watch Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand for luxury accessories from millennial consumers | +1.5% | Global, with stronger impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +1.2% | Global, with significant impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing strategic investment and initiatives propelling the market | +0.9% | Global, with concentration in Europe and North America | Medium term (2-4 years) |

| Growing interest in vintage and pre-owned luxury watches | +0.8% | Global, with stronger impact in North America and Europe | Short term (≤ 2 years) |

| Product innovation in terms of raw material and design | +0.7% | Global, with stronger impact in Europe and North America | Long term (≥ 4 years) |

| Rising consumer awareness about watch craftsmanship and heritage | +0.6% | Global, with stronger impact in Europe and North America | Medium term (2-4 years) |

Source: Mordor Intelligence

Strong Demand For Luxury Accessories From Millennial Consumers

Millennials significantly influence the global luxury watches market through their distinct consumer behavior. This demographic views luxury timepieces as both functional items and symbols of personal achievement and social status. Social media platforms substantially impact their purchasing decisions by providing channels to showcase luxury acquisitions. Millennials demonstrate particular attention to manufacturing quality, brand reputation, and environmental sustainability, leading to selective purchasing patterns and increased demand for corporate transparency. In the United States, the growing millennial population supports this market demand. According to the US Census Bureau, millennials represented the largest generational group in 2024, comprising 21.8% of the United States population. Their preference for technical excellence and design quality has led luxury watch manufacturers to adapt their strategies, including limited editions, exclusive collections, and personalization options that align with modern preferences. This trend is evident in recent product launches, as demonstrated by Tissot's introduction of the Supersport NBA Special Edition as the 2025 Official Watch of the NBA in February 2025, featuring a 45.5 mm stainless steel case, lugs, crown, and two chronograph pushers.

Influence of Social Media and Celebrity Endorsement

Social media platforms and celebrity endorsements have transformed the luxury watches market by revolutionizing brand-consumer connections and purchase behaviors. Instagram, Facebook, and YouTube's visual-focused platforms enable luxury watch brands to showcase detailed craftsmanship and design through high-quality imagery and brand storytelling. Facebook remains the most widely used social network globally, with 3.06 billion monthly active users as of Q4 2023, according to Meta Platforms [1]Source: Meta Platforms, "Number of monthly active Facebook users worldwide,"meta.com. Influencer marketing has significantly impacted the industry, with both major celebrities and micro-influencers providing authenticity and aspirational value to watch brands through their social media presence. This approach particularly resonates with younger, digital-native consumers who value influencer recommendations over traditional advertising. The impact of celebrity partnerships extends further as they represent the lifestyle and prestige of luxury timepieces. Consumer-generated content, including personal collections and experiences, strengthens brand communities and authenticity. Social commerce features facilitate direct purchasing from inspiration. Many luxury watch companies have responded by establishing celebrity partnerships. In September 2024, Anushka Sharma collaborated with Michael Kors to create a limited-edition timepiece, becoming the first female Indian celebrity to launch a commercially available signature watch in India.

Increasing Strategic Investment and Initiatives Propelling the Market

The global luxury watch market continues to evolve through investments in innovation, market development, and adaptation to consumer preferences. Companies are incorporating technological advancements, including artificial intelligence, luxury smartwatches, and personalized customization options to appeal to younger, tech-savvy consumers worldwide. Through international partnerships, collaborations, and acquisitions, companies expand their product portfolios, enhance distribution networks, and penetrate emerging markets, particularly in Asia and the Middle East, where rising disposable incomes and urbanization fuel market growth. This strategic approach is exemplified by leading manufacturers like Rolex, Patek Philippe, and Audemars Piguet, who control their production volumes and release limited editions to maintain scarcity and exclusivity, thereby increasing value in both primary and secondary markets. For instance, in February 2025, Rolex expanded its retail presence by opening a new 650-square-foot boutique at DLF Emporio, New Delhi, in partnership with Kapoor Watch Company. This location serves as a showcase for Rolex's watch collection in India's capital city. These developments indicate the industry's commitment to strategic global expansion while maintaining brand exclusivity and market value.

Product Innovation in Terms of Raw Material and Design

The luxury watch market's production innovation is driven by advances in materials and design, setting new benchmarks for quality, sustainability, and exclusivity. Manufacturers are incorporating high-tech materials, including titanium, ceramic, carbon fiber, and proprietary alloys, which combine the durability of modern composites with precious metals. The industry's sustainability efforts include recycled metals, lab-grown gemstones, and vegan straps, along with production processes powered by renewable energy. Companies have implemented circular economy practices through certified pre-owned programs. Design innovations feature expanded color selections, transparent cases, and customization options allowing customers to choose dial colors, engravings, and complications. While manufacturing processes incorporate automation, robotics, and 3D printing for improved precision and prototyping, traditional hand-finishing methods like guillochage and perlage remain essential. Companies continue to protect their technological advances through patents. In August 2024, Rolex secured a patent for a digital system that stores and accesses watch service history. This system utilizes NFC-enabled warranty cards that, when scanned, provide access to a web platform displaying service records and additional information. The patent includes provisions for QR codes, RFID tags, and barcodes as alternative data access methods.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartwatch adoption challenges traditional timepiece sales | -0.9% | Global, with stronger impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Proliferation of counterfeit products | -0.8% | Global, with higher impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| High import tariffs increase retail prices globally | -0.7% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Lesser demand from price sensitive consumers | -0.5% | Global, with stronger impact in emerging markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Proliferation of counterfeit Products

As counterfeit products proliferate, the global luxury watch market grapples with mounting challenges, spurring urgent regulatory interventions and unified industry actions. These fakes not only tarnish brand reputation and diminish consumer trust but also inflict hefty financial damages. A case in point: On May 4, 2025, U.S. Customs and Border Protection (CBP) in Chicago intercepted a shipment from China, containing 243 counterfeit luxury watches. The haul boasted fakes of renowned brands like Rolex, Patek Philippe, Cartier, and Omega, with a staggering estimated retail value surpassing USD 6.6 million[2]Source: U.S. Customs and Border Protection, “1Shipment: 243 Fake Designer Watches Worth Over USD 6 Million Seized by CBP Officers in Chicago,”cbp.gov. Once rudimentary, the counterfeit industry has now mastered the art of crafting high-precision replicas, often eluding the keen eyes of seasoned collectors and authentication experts. Such advancements not only dampen the resale value of genuine timepieces but also sow doubt among buyers regarding product authenticity. The growing sophistication of counterfeit operations has forced luxury watchmakers to innovate and invest heavily in anti-counterfeiting measures. In addition to blockchain-based solutions, companies are exploring advanced technologies like micro-engraving, invisible ink, and AI-driven authentication tools to safeguard their products. These efforts aim to protect brand integrity, reassure consumers, and maintain the exclusivity that defines the luxury watch market. In a bid to combat this, luxury watchmakers are turning to blockchain technology, implementing digital passports that trace ownership history and product origin.

Lesser demand from price sensitive consumers

Economic uncertainties have heightened price sensitivity across consumer segments, particularly affecting the luxury watch market due to its discretionary nature and high price points. The market faces significant challenges as rising retail prices, driven by increased production costs, tariffs, and higher precious metal prices, make these products less accessible to many potential buyers. The continuous price increases by luxury watch brands have resulted in weakened demand, as these discretionary purchases become more susceptible to changes in consumer sentiment and economic conditions. The secondary market reflects these challenges through declining pre-owned watch prices from their peak levels. Market inventories have grown, and buyers have become more selective, either waiting for better deals or returning to authorized dealers instead of paying premium prices. While brands focus on ultraluxury buyers and limited editions to offset reduced volume from price-sensitive segments, this strategy has not fully compensated for the overall decline in demand. This market contraction is evident in Swiss watch exports, which decreased by 3.3% during the first six months of the year compared to January-June 2023, according to the Federation of the Swiss watch industry [3]Source: Federation of the Swiss Watch Industry, “Swiss Watch Exports in the First Half of 2024,” fhs.swiss .

Segment Analysis

By Product Type: Heritage Meets Technology

In 2024, the quartz/mechanical watch segment constitutes 63.85% of the global luxury watch market, demonstrating its market prominence through technical precision and established heritage. According to the Federation of the Swiss Watch Industry's official data, mechanical watches demonstrated a 7.0% expansion in export value during 2023, contributing approximately 80% to the total export turnover growth. This substantial market performance reflects international consumer confidence in Swiss manufacturing standards and high-precision mechanical timepieces. The segment maintains its dominant market position through the strategic development of quartz-mechanical hybrid timepieces, emphasizing structural integrity and traditional craftsmanship, particularly across established markets including Europe, North America, and the Asia-Pacific regions.

The digital watch segment demonstrates significant growth potential with a projected CAGR of 6.42% during 2025-2030, surpassing the anticipated growth rate of the broader luxury watch market. This expansion corresponds directly to evolving consumer preferences among the Millennial and Generation Z demographics, who demonstrate increased demand for technology-integrated luxury timepieces. These consumer segments prioritize digital and hybrid watches, incorporating advanced functionalities, including health monitoring systems, mobile device integration, and customization capabilities. Luxury watch manufacturers are responding through the strategic implementation of advanced technological features within premium design frameworks. For instance, in August 2023, Urban introduced their Luxury Edition smartwatches - Urban Titanium, Urban Dream, and Urban Rage, combining technological capabilities with premium design.

By End User: Women Drive Future Growth

The luxury watch market shows a distinct gender distribution, with men holding a 51.88% market share in 2024. This dominance stems from cultural, aesthetic, and historical factors that have established luxury watches as status symbols for men. Luxury timepieces serve as expressions of personal taste and indicators of success, professionalism, and affluence, particularly within male-dominated executive and collector communities. The prevalence of larger case sizes, complex complications, and minimalist designs aligns with male consumer preferences, reinforcing this demographic's lead. Luxury brands have primarily focused their flagship designs on male aesthetics and performance-oriented engineering, establishing their position in the male luxury lifestyle segment. In January 2025, Rolex introduced the Oyster Perpetual Land-Dweller for men, featuring distinctive aesthetics and advanced technology, available in 36 mm and 40 mm sizes.

The women's luxury watch segment demonstrates the fastest growth, with a projected CAGR of 6.75% from 2025 to 2030, surpassing overall market expansion. This growth reflects evolving consumer demographics and brand strategies, driven by increasing female economic empowerment in the luxury market. Rising financial independence and the growing influence of women in corporate and entrepreneurial sectors contribute to higher discretionary spending on premium lifestyle goods, including luxury watches. Female workforce participation serves as a fundamental driver of this growth. For instance, in Japan, the female employment rate reached 54.2% in 2024, according to the Ministry of Internal Affairs and Communications [4]Source: Ministry of Internal Affairs and Communications, “Labour Force Survey: Female Labour Force Participation Rate Reaching 54.2% in 2024,”stat.go.jp

. This trend indicates a broader global pattern where increased professional engagement among women correlates with higher demand for high-end timepieces as both fashion statements and professional accessories.

By Distribution Channel: Digital Transformation Accelerates

In 2024, global luxury watch sales saw offline retail stores commanding a dominant 66.82% share. This stronghold is largely attributed to the tactile and immersive experience in-store shopping offers, crucial for assessing craftsmanship, materials, and mechanical intricacies. Prestigious boutiques, such as Patek Philippe’s Salons in Geneva and Rolex’s flagship outlets, not only grant exclusive product access but also deliver personalized services within an esteemed brand environment. Multi-brand luxury retailers, including Watches of Switzerland and Cortina Watch, amplify this in-store allure by curating collections and providing expert consultations. Luxury watchmakers are doubling down on physical retail investments; for instance, Omega is revamping its boutiques for a more experiential touch, while Audemars Piguet is establishing 'AP Houses' that weave brand storytelling with top-tier service.

On the other hand, online retail is emerging as the fastest-growing channel, boasting a projected CAGR of 7.01% from 2025 to 2030. A pronounced shift towards digital-first strategies fuels this surge. Brands such as Cartier and TAG Heuer are leading the charge with offerings like virtual try-ons and online concierge services. Simultaneously, industry giants Rolex and Breitling are broadening their horizons by collaborating with platforms like Chrono24 and WatchBox, enhancing their certified pre-owned selections. Digital storefronts are also making waves, with LVMH debuting its Watch Week online showcase and Richemont seamlessly integrating with Yoox Net-a-Porter. These digital initiatives strike a chord with the younger, tech-savvy demographic, who prioritize transparency, convenience, and reliable authentication in the luxury e-commerce landscape.

Geography Analysis

Asia-Pacific holds a 40.51% share of the luxury watch market in 2024, driven by the region's expanding affluent population and cultural emphasis on luxury goods as status symbols. The market growth in Asia-Pacific stems from increased disposable income and evolving consumer preferences, particularly in China, India, and Japan. Global luxury brands are expanding their presence in these countries due to market potential. China leads the regional market due to its substantial high-net-worth population, contributing significantly to Asia-Pacific's market dominance.

South America is projected to grow at a CAGR of 7.63% from 2025 to 2030. This growth is attributed to increased wealth creation, urbanization, and an expanding high-net-worth population seeking luxury items as status symbols. Digital platforms and e-commerce adoption enhance market accessibility for urban consumers. Mechanical watches are increasingly popular as investment pieces and status symbols, while electronic watches generate the highest revenue. International brands are expanding their regional presence to capitalize on evolving consumer preferences and demand for Swiss and European timepieces.

Europe retains its traditional importance in the luxury watch market, with Switzerland, France, and Italy functioning as key production and consumption centers. While tourism drives sales, global travel variations affect market stability. North America, especially the United States, represents a mature market with consistent demand for heritage mechanical watches and luxury smartwatches. The region shows growing interest in independent watchmakers and limited editions. The Middle East and Africa region offers expansion opportunities, with the United Arab Emirates and Saudi Arabia emerging as luxury centers, particularly in the ultra-luxury segment due to their concentration of ultra-high-net-worth individuals.

Competitive Landscape

The luxury watch market exhibits moderate consolidation in its premium segment, with companies like Rolex SA, Compagnie Financière Richemont S.A., The Swatch Group Ltd, LVMH Moët Hennessy Louis Vuitton SE, and Richard Mille SA dominating the market. These companies maintain their positions through strong brand equity and manufacturing expertise. Their competitive strategies focus on product differentiation, heritage-based positioning, and strict distribution channel control rather than price competition. For instance, LVMH's Hublot brand introduced three new Big Bang Chronograph models in January 2025, featuring Sand Beige, Dark Green, and Sky Blue ceramic cases. Each model is limited to 200 pieces, marking the first time these colors are available in the Big Bang collection.

The accessible luxury segment presents significant market expansion opportunities, particularly in capturing first-time luxury watch consumers across global markets. While the direct-to-consumer digital channel remains underdeveloped compared to other luxury market segments, independent watchmakers are establishing strong market positions through targeted social media strategies and digital-first customer acquisition approaches. This strategic shift enables these manufacturers to optimize marketing expenditure while building direct relationships with consumers across international markets.

Additionally, technology-oriented luxury manufacturers are developing premium smartwatch offerings that integrate traditional luxury elements with contemporary functionality. Market participants are implementing comprehensive technological solutions across their operations, including blockchain technology for enhanced product authentication and supply chain transparency, artificial intelligence systems for detailed consumer behavior analysis and personalization, and augmented reality platforms for immersive virtual product demonstrations and customer engagement.

Luxury Watch Industry Leaders

-

Rolex SA

-

Compagnie Financière Richemont S.A.

-

The Swatch Group Ltd

-

LVMH Moët Hennessy Louis Vuitton SE

-

Richard Mille SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Citizen introduced a new product category, Citizen Premiere, for its luxury timepieces. The collection combines design and technology elements to establish a position in the modern luxury watch segment.

- October 2024: Jacob & Co. partnered with Cristiano Ronaldo to launch an exclusive luxury watch collection. The Twin Turbo Furious Baguette, a standout design from this collaboration, was personally delivered.

- August 2024: Ethos opened a new store, Ethos Summit, at Phoenix Mall of Asia in Bengaluru. The boutique offers a selection of luxury watches to customers.

- April 2024: Chopard launched new timepieces for men and women, featuring the L.U.C XPS Forest Green and the Alpine Eagle XL Chrono models. The company incorporated its proprietary alloy, which contains at least 80% recycled materials and offers enhanced technical properties. These watches utilize the in-house L.U.C Calibre 96.12-L movement.

Global Luxury Watch Market Report Scope

Luxury watches are timepieces that go beyond simple timekeeping, offering exceptional craftsmanship, high-quality materials, and often unique designs. The luxury watch market is segmented into product type, end-user, distribution channel, and geography. By product type, the market is segmented into quartz/mechanical watches and digital watches. By end user, the market is segmented into men, women, and unisex. By distribution channel, the market is segmented into offline stores and online stores. The report also provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| By Product Type | Quartz/Mechanical Watch | ||

| Digital Watch | |||

| By End User | Men | ||

| Women | |||

| Unisex | |||

| By Distribution Channel | Offline Stores | ||

| Online Stores | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Quartz/Mechanical Watch |

| Digital Watch |

| Men |

| Women |

| Unisex |

| Offline Stores |

| Online Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected luxury watch market size by 2030?

The luxury watch market is expected to reach USD 72.98 billion by 2030, supported by a 6.14% CAGR.

Which region leads the luxury watch market today?

Asia-Pacific holds the largest regional position with 40.51% of global revenue in 2024, anchored by China, Japan, and India.

Why are digital watches gaining ground in the luxury segment?

Hybrid models that blend premium materials with discreet smart functions deliver additional health and connectivity value, driving a 6.42% CAGR for digital watches through 2030.

How important is the women’s segment to future growth?

Women’s demand is forecast to rise at 6.75% CAGR, outpacing the overall market as brands introduce dedicated designs and complications.